Koho Wins a Global Recognition Award 2026

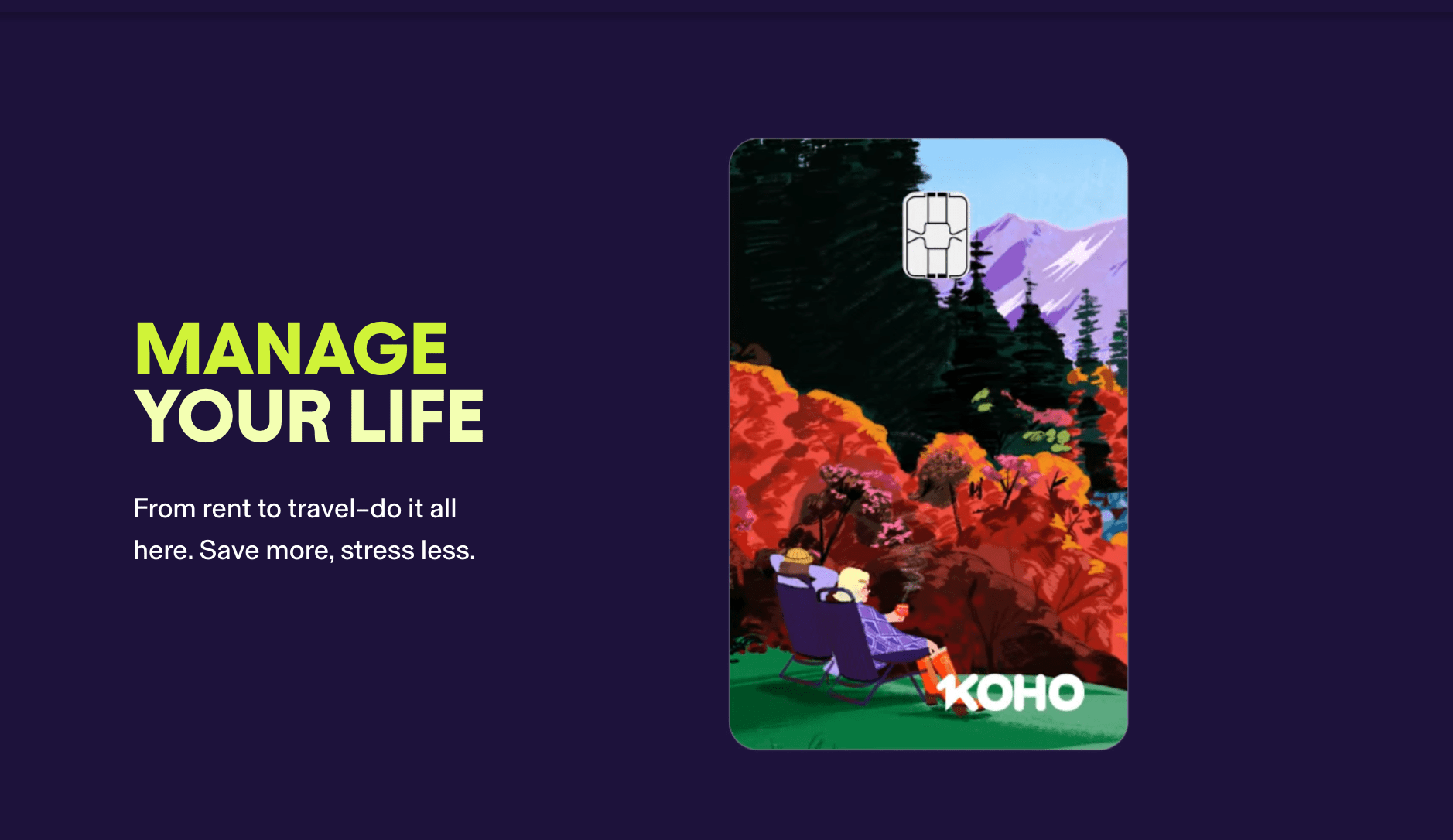

A 24-year-old newcomer to Canada works two jobs while saving for a security deposit and building a credit history, facing difficult choices: Big Five banks require minimum balances of $3,000 to avoid $15 monthly fees, traditional credit cards demand credit scores that newcomers lack, and payday lenders charge 400% annual interest for emergency cash. Before KOHO, this scenario meant choosing between extractive fees, credit access barriers, or financial exclusion. Instead, she downloads KOHO’s mobile app, opens an account with instant approval, receives a prepaid Mastercard earning 1% cash back on groceries and transit, earns 2% interest on her entire balance with no minimums or monthly fees, subscribes to Cover for $2 monthly providing $250 emergency cash without credit checks, uses the $5 monthly credit building product seeing her score increase 31+ points in four months, and pays rent through KOHO with automatic reporting to Equifax building credit history. This transformation explains why KOHO, a Canadian neobank challenger, has won the 2026 Global Recognition Award for democratizing financial services through subscription-based banking, making wealth creation accessible to underserved Canadians. Founded in 2014 by Daniel Eberhard (serial entrepreneur who sold renewable energy company Kineticor), KOHO achieved 2 million+ users, $800 million valuation, $100 million+ revenue run rate, and acceptance into Phase II of Schedule 1 bank license application.

Technical Innovation and Architecture

KOHO’s subscription-based model offers tiered plans delivering progressively higher value: Essential ($0 monthly) provides 1% cash back on groceries, transit, and dining plus 2% interest on entire balance with no account minimums or monthly fees generating over $100 yearly in value; Extra ($12 monthly) increases cash back to 1.5%, interest to 2.5%, eliminates foreign transaction fees, and discounts credit building 30% generating over $200 yearly in value; Everything ($14.75 monthly) maximizes cash back at 2%, interest at 3.5% (highest among Canadian neobanks), includes all Extra benefits plus 50% credit building discount, advanced phone support, and lifestyle perks generating over $500 yearly in value. This transparent pricing contrasts with the Big Five banks, which charge $10-30 monthly for basic accounts that pay near-zero interest. The 3.5% interest applies automatically to the entire account balance without requiring transfers to separate savings accounts, simplifying wealth accumulation.

Cover, KOHO’s cash advance product, provides up to $250 in instant liquidity for a $2+ monthly subscription with no credit checks, penalties, or late fees, unlike payday lenders, which charge 400% annual interest. The system includes personalized advice from certified Financial Coaches, valued at over $80 per session, and automatically replenishes the available balance when members add funds, creating a revolving credit facility. The August 2024 launch of Rent Reporting integrated automation reports rental payments directly to the Equifax credit bureau when members pay rent through KOHO, seamlessly building credit history without manual reporting or third-party fees that typically cost $50-100 annually. The system includes historical rent payment reporting and automatic payment processing. All plan members with Tenant Insurance coverage receive a 0.25% cash-back bonus on rent payments, which creates positive reinforcement.-back bonus on rent payments, which creates. The credit-building products enable members to deposit $30-$500 as security, borrow against it, and build credit through on-time payments, averaging 31+ point score increases in four months, addressing the catch-22 where youth, immigrants, and those rebuilding credit need credit history to access credit.

Market Strategy and Leadership

Daniel Eberhard, founder and CEO, co-founded Kineticor Renewables in 2010 during business studies at Mount Royal University, developing $50 million in wind energy projects before selling to Algonquin Power & Utilities in 2011. Following the exit, Eberhard spent several years as angel investor and mentor before founding KOHO in December 2014 after recognizing that “the number one investment product sold in Canada will eat up 30-50% of a citizen’s retirement” through mutual fund fees, while “two-thirds of Canadians don’t have enough for account minimums that big 5 banks require to avoid fees.” His personal experience growing up with a single mother “who worked very hard, drove buses, cleaned houses” drives KOHO’s mission: “Democratizing access to wealth creation means giving people financial security to spend more time with family, own a home, or save for tuition for their grandkids.”

KOHO raised C$486 million in equity and a C$150 million debt facility. The February 2022 Series D raised C$210 million, led by Eldridge, with existing investors Drive Capital and TTV Capital, as well as HOOPP, Round13, and BDC. The December 2023 Series D extension raised C$86 million at a $800 million valuation, maintaining a flat valuation amid declining valuations for most Canadian fintechs. Drive Capital partner Chris Olsen stated, “KOHO is emerging as the winner in Canada” among challenger banks. The October 2024 round secured C$190 million (C$40 million in equity, C$150 million in debt), led by PROPELR Growth and new investor Rockefeller Capital, to fund lending expansion and pursue a bank license. Eberhard stated: “We had the choice of profitability with our existing capital, but this injection allows us to grow faster and expand our lending business, both of which support our bank license application.” User base grew from 500,000 (early 2022) to 1 million+ (December 2023) to 2 million+ (February 2026), achieving $100 million+ revenue run rate (doubled year-over-year) with “hundreds of millions” in loan book. The January 2024 acceptance into Phase II of the Schedule 1 bank license application positioned KOHO to become the first fintech-native bank in Canada.

Industry Impact and Future Vision

KOHO addresses fundamental Canadian banking inefficiencies: Big Five banks charging $10-30 monthly account fees while paying near-zero interest, credit building barriers creating a catch-22 for youth and immigrants, rental payments not building credit disadvantaging 40% of Canadians who rent, payday lenders, charging predatory 400% annual interest for emergency cash, and fragmented financial services requiring multiple institutions. By offering prepaid Mastercard with up to 2% cash back, 3.5% interest on entire balance, Cover cash advances for $2+ monthly with no credit checks or penalties, credit building products averaging 31+ point score increases, automatic Rent Reporting to Equifax, Tenant Insurance at competitive $22 monthly, no foreign transaction fees, and integrated lifestyle services (eSIM, Travel Insurance), KOHO provides comprehensive financial hub at transparent subscription cost saving typical members hundreds to thousands annually versus traditional banks.

The white-label infrastructure business powering Wealthsimple Cash card demonstrates technical credibility and diversified revenue streams. CEO Eberhard emphasizes efficiency: “The team’s small today, it’s 250 people, it will probably always be 250 people, and we get to ship all these great products and create all these savings and pass those on to the user in the form of better savings rates or better cash back.” With 2 million+ users achieving #1 Canadian financial app ranking with 4.8 App Store rating, $800 million valuation maintained through 2023 downturn, C$486 million+ equity plus C$150 million debt, $100 million+ revenue run rate approaching profitability, Phase II bank license acceptance positioning as first fintech-native Schedule 1 bank, 3.5% interest on entire balance highest among neobanks, Rent Reporting building credit for renters, white-label infrastructure powering Wealthsimple, Cover providing ethical emergency liquidity, and mission-driven financial inclusion focus, KOHO has established itself as Canada’s leading neobank challenger transforming banking for millennials, Gen Z, newcomers, and underserved segments. These achievements demonstrate why KOHO has earned the 2026 Global Recognition Award for its contribution to financial democratization and technological innovation in consumer banking.

AWS-Native Ecosystem: Operates 100% on Amazon Web Services, utilizing Amazon EKS for automated, zero-touch container operations.

AI Integration: Holistically embeds Large Language Models (LLMs) to provide secure, real-time financial coaching and automated support.

Cloud Cost Efficiency: Achieved a 30% reduction in infrastructure costs through the implementation of EKS Auto Mode.

Real-Time Analytics: Utilizes Google BigQuery for high-speed data warehousing and advanced financial pattern recognition.

Machine Learning Stack: Employs scikit-learn and NumPy to power proprietary credit-scoring and fraud-detection algorithms.

Cybersecurity Standard: Adheres to the NIST Cybersecurity Framework to ensure bank-grade protection for 2M+ users.

User Growth: Surpassed 2 million active users in the Canadian market by early 2026.

High Run Rate: Generates an estimated revenue run rate exceeding $100 million as of the last fiscal reporting.

Lean Engineering: Maintains a high user-to-employee ratio by automating 90% of routine infrastructure tasks.

Payment Registration: One of the first fintechs to become a registered Payment Service Provider with the Bank of Canada.

Geographic Expansion: Successfully launched international money transfer services reaching over 190 countries.

Rapid Deployment: Maintains a high-velocity product cycle, recently launching joint accounts and in-app bill splitting.

Series D Funding: Secured $86 million in extension funding in December 2023 to fuel aggressive expansion.

Significant Valuation: Valued at approximately $800 million, positioning it as a near-unicorn in the Canadian fintech sector.

Top-Tier Investors: Backed by industry leaders including Drive Capital, Portage, BDC, and Rockefeller Capital Management.

Postal Banking Alliance: Partnered with Canada Post to offer physical banking access to rural and underserved populations.

Award Recognition: Ranked #2 on Deloitte’s 2025 Technology Fast 50 list for outstanding growth and innovation.

Banking License Pursuit: Actively moving through regulatory stages to obtain a full Canadian banking license.

Zero-Fee Model: Solves the primary pain point of high Canadian banking fees with a no-fee daily chequing alternative.

Instant Credit Building: Offers an in-app Credit Building tool that allows users to improve their scores through spending.

Seamless Onboarding: Enables users to set up a full spending and savings account in under three minutes via mobile.

High User Engagement: Maintains high app store ratings and an internal mission-alignment score of 4.6/5.

Integrated Rewards: Provides instant cash back on purchases through a proprietary Mastercard partnership.

Universal Accessibility: Offers multi-currency support and e-SIM features for travelers and international users.

Financial Inclusion: Specifically targets the “underbanked” and those excluded by traditional minimum balance requirements.

Ethical AI Governance: Implements strict data privacy and bias mitigation protocols in its automated lending models.

AI for Good: Focuses development on tools that promote “Financial Progress” rather than predatory debt cycles.

Remote-First Culture: Operates a fully remote workforce across 6 continents, reducing the corporate carbon footprint.

Transparent Finance: Maintains a “User First” value system, prioritizing fee transparency and data ownership.

Government Collaboration: Partnered with the CRA to ensure efficient delivery of social benefits to vulnerable citizens.